For those who are accumulating funds for a child’s or grandchild’s education expenses, there was good news in the American Taxpayer Relief Act of 2012, which was passed to avoid the “fiscal cliff” as this year started. The tax code provisions for the Coverdell Education Savings Account (ESA) were made permanent, removing a cloud of uncertainty. These accounts may be an alternative to or a supplement to a 529 college savings plan.

Contributions to 529 plans and ESAs are not tax deductible, but there is no tax as the income builds up in the account. Distributions from the plans are tax free if they are used for qualified education expenses. The definition of what qualifies is not the same for the two approaches.

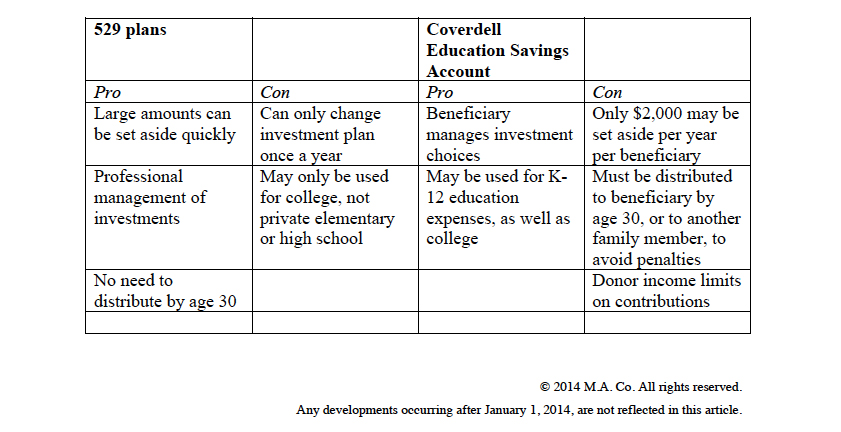

ESAs have two advantages over 529 plans. First, qualified expenses are not limited to higher education, as with the 529 plan, but may also include tuition at private school as early as kindergarten. Second, where 529 plans are typically limited to just a few investments choices, with the money managed by the plan sponsor, there are no similar limitations for ESAs.

However, there are ESA disadvantages to consider also, where the 529 plan is superior. Most importantly, no more than $2,000 per year per student may be contributed to an ESA. Second, contributions must end when the beneficiary reaches age 18. Therefore, no more than $36,000 total may be set aside for one student, which almost certainly will fall far short of the financial need. Still, having a dedicated capital source that is growing tax free as one begins higher education is nothing to sneeze at.

A third problem is that contributions to ESAs are not permitted for those whose income is too high—modified adjusted gross income of $110,000 for singles, $220,000 for a married couple. No similar limitation applies to the 529 plan.

Successor beneficiaries

What if the beneficiary decides against college? The ESA accumulation may be rolled into another ESA for a family member of a beneficiary, or an new beneficiary may be designated for the 529 plan. The new beneficiary must be of the same or higher generation as the original beneficiary.

The ESA must be distributed by the time the beneficiary reaches age 30, or within 30 days after that date. The distribution may be in the form of a rollover to another family member. Amounts not rolled over and not used for qualified expenses are included in taxable income, and a 10% tax penalty applies. No such age limits apply to the 529 plan.

Start early

As valuable as the tax advantages of ESAs and 529 plans may be, the biggest advantage is starting early. The sooner one begins setting aside funds for a college education, the more time that capital has to grow into something significant.