One important goal of the Patient Protection and Affordable Care Act (PPACA) was to guarantee health insurance availability regardless of health status, eliminating rejections due to pre-existing conditions. The practical problem with such a guarantee is that some people may find it in their self-interest to avoid the expense of health insurance, waiting until they are really sick and buying it then. That shrinks the pool of premium payers, driving up the costs for those who do have insurance. The remedy to that problem is the individual mandate.

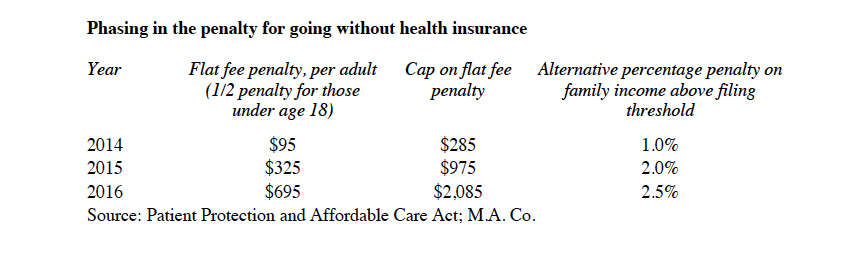

Beginning in 2014, most Americans will have to demonstrate to the IRS that they have adequate health insurance. Failure to have adequate health insurance triggers an additional income tax payment to the government. The law called the payment a penalty. Chief Justice Roberts called it a tax in order to join a majority of U.S. Supreme Court Justices sustaining the constitutionality of the PPACA. The initial penalty is relatively low, but it very roughly doubles and redoubles as shown in the table below. The penalty is the greater of a flat fee or a percentage of family income above the income tax filing threshold. A penalty payment is owed for each uninsured adult in a family, and a half penalty is owed for each child under age 18, but the flat fee is capped at three times the base penalty. That corresponds to two adults and two minor children. After 2016 the penalty is adjusted annually for inflation.

“Family income” for purposes of the percentage penalty is the taxpayer’s modified adjusted gross income (MAGI) plus the MAGI of any other family members for whom the taxpayer claims an exemption, plus any tax-exempt interest received during the tax year. Social Security benefits not included in gross income are not counted.

Example. Assume a single taxpayer has $50,000 of MAGI and that the filing threshold is $10,000. The excess income is $40,000, so the 1% penalty in 2014 comes to $400, and the 2% penalty in 2015 would be $800. Those would be payable, as they are higher than the flat fee. Generally, the annual penalty will be capped at an amount equal to the national average premium for qualified health plans that have a “bronze” level of coverage available through the state exchanges.

Exemptions

There are nine statutory exemptions from the enforcement of the penalty imposed by the individual mandate:

Religious conscience. Members of religious sects recognized as opposed to insurance. The Social Security Administration administers a process for identifying and recognizing these religious organizations. Members will need to apply for an exemption certificate from a Health Insurance Marketplace.

Health care sharing ministry. Members of recognized health care sharing ministries.

Indian tribes. Members of federally recognized Indian tribes.

Incarceration. Those who are currently incarcerated.

Not lawfully present. Persons who are not U.S. citizens or U.S. nationals, or who are aliens not lawfully present in the U.S.

Not required to file tax returns. Those whose income falls below the income tax filing threshold. The threshold is a function of filing status, age, and types and amounts of income. Thresholds are expressed in terms of gross income. In 2012 the filing threshold for single taxpayers under age 65 was $9,750, and for married couples filing jointly (both under age 65), it was $19,500.

Short coverage gap. The penalty imposed by the individual mandate applies on a monthly basis. Someone who changes jobs and has a coverage gap of less than three consecutive months is excused from the penalty. A month of coverage is any month in which the taxpayer had health insurance coverage for a single day.

Hardship. A Health Insurance Marketplace, also known as an Affordable Insurance Exchange, may issue hardship certificates to those unable to obtain coverage.

Unaffordable coverage options. If the available coverage requires premium payments in excess of 8% of household income, it is considered unaffordable, and the taxpayer does not have to buy it.

In general, an exemption from the individual mandate will be claimed as part of filing a federal income tax return.

Senior citizens

The individual mandate applies to senior citizens, but Medicare qualifies as minimum essential coverage. Each month of Medicare participation counts toward the mandate.

Enforcement

The requirement to have health insurance begins on January 1, 2014, and will be reported to the IRS on 2014 Forms 1040 in early 2015. Much could change before then. The Obama administration already has announced that it won’t enforce the employer mandate in 2014, and there is political pressure to extend that waiver to individuals also. IRS enforcement tools have been deliberately limited by the PPACA. Specifically, the IRS is only authorized to withhold the penalty under the individual mandate from a taxpayer’s income tax refunds, which are received by roughly half of all taxpayers each year. If a taxpayer has no refund due, then current law would result in a de facto avoidance of the penalty under the individual mandate. Last year the Congressional Budget Office estimated that by 2016 about 11 million taxpayers would be subject to the individual mandate and about 6 million would choose to pay the penalty, raising $7 billion in revenue.

However, anecdotal evidence suggests that taxpayers likely will alter the way in which they withhold for taxes in order to ensure that they do not owe taxes at the end of the year, or come as close to zero as possible, in order to avoid the penalty associated with the individual mandate. In this way, taxpayers could obtain health insurance at a moment’s notice when sickness arises (due to the PPACA’s prohibition against denials due to pre-existing conditions) rather than carrying escalating premium insurance during periods of health. One of the goals of the PPACA was to dilute the insurance pool with healthy individuals who normally do not access their care, thereby reducing premium costs across the board. If a large number of normally healthy individuals avoid the penalty under the individual mandate by under-withholding, the costs for premiums will increase rather than decrease for those remaining on the insured rolls.

© 2014 M.A. Co. All rights reserved.

Any developments occurring after January 1, 2014, are not reflected in this article.