Life insurance is surely one of the most versatile and important tools in estate planning. Not only can it provide for a family’s welfare in the event of the untimely death of the breadwinner, but insurance proceeds also can pay estate taxes, leaving legacies intact for the heirs.

The drawback to using life insurance to pay estate taxes is that the insurance death benefit itself is included in the estate and, therefore, increases the amount of tax the estate must pay.

Fortunately, this situation is only true if the decedent were the owner of the insurance policy. When the policy belongs to a beneficiary or a third party, its proceeds never become part of the estate. To accomplish this, the decedent must have surrendered every vestige of ownership at least three years prior to the date of death.

This can be done simply by turning the policy over to a trusted person. Annual gifts can be made to that person to cover the premiums. However, the new owner will control the policy. He or she can change beneficiaries, neglect to make premium payments, even surrender the policy for its cash value.

Insurance can provide for the survival of a closely held business. Suppose that one child works in the business and is best qualified to run it, but the business is the estate’s major asset. An insurance policy can provide fair shares to the other heirs, leaving the business child to manage the enterprise without interference.

Insuring two (or more) lives

When an estate passes to a husband or wife, no tax is due. However, upon the survivor’s death, the IRS may claim a substantial share of large estates. Married couples can provide for payment of estate taxes most economically with second-to-die, or survivorship, life insur¬ance. Because the death benefit is payable only on the death of the second spouse, this type of policy carries a lower premium than a single policy—and much lower than two individual policies. Savings of 50% or more may be possible, depending on age and insurability.

The insurance industry also offers first-to-die policies, which cover two or more lives but pay only upon the first death. A working husband and wife can use this type of coverage to ensure that money to replace lost earnings will be available to the survivor and the children.

First-to-die insurance also can be useful in protecting a family business or a business partnership. It can supply the extra cash needed for a business to recover from the effects of a key member’s death. Or the insurance can provide partners or family members with the money to complete a buy-sell agreement.

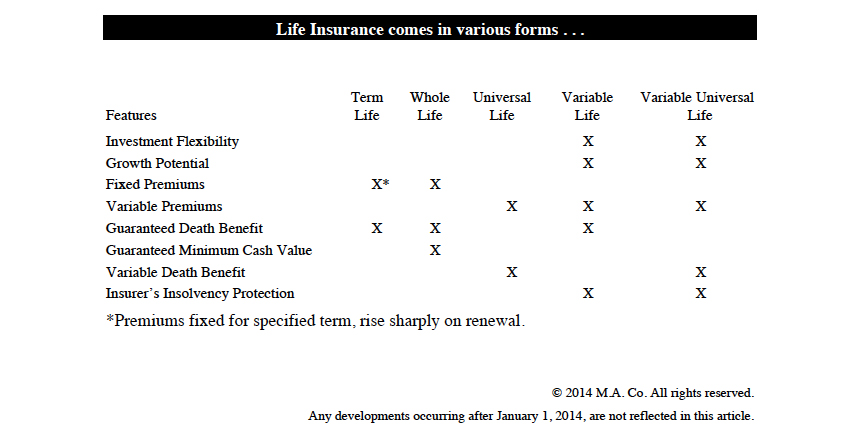

Choosing a policy

Today life insurance is offered in several different packages, each with its own advantages and disadvantages. The table here summarizes the features of the major types. Premiums can vary widely—as can the solvency of insurance companies. So it pays to shop, and to ask questions.

Insuring a business

In addition to life insurance, a business owner or professional needs to insure against a wide range of risks. Of course, the needs of each business are unique. Coverages should be reviewed periodically to ensure that continuation of the business is not at risk.

Property insurance protects against fire and smoke damage, but owners may also need to consider the possibility of losses from floods, hurricanes, earthquakes, building collapse and other unforeseen events. Such disasters usually bring extra costs—such as cleanup, storage, rentals and repairs—that can be covered by insurance. And policies are available to cover the cost of lost business.

Liability insurance can simply cover persons injured on the business premises or by its employees. Professional liability insurance, also known as “errors and omissions” or “malpractice” insurance, is available for architects and engineers as well as doctors, lawyers, accountants, brokers and other licensed professionals. And an umbrella policy can cover large liabilities after the basic coverage maxes out.

And that just may be the beginning of the insurance needs of a going business. Insurance may cover employee bonding and employee dishonesty. Workers’ compensation is mandatory, and health insurance may be essential in attracting and retaining qualified employees. Now it’s even possible to insure commercial receivables.

Many insurance companies also offer a special combined policy known as a business owner’s policy (BOP). Although not available to certain types of business, such as auto repair shops and restaurants, BOPs can offer small businesses comprehensive protection at a price well below the cost of buying the most important coverages separately.